The Belgian tax reform

End July, the Belgian Government issued a plan to overhaul the Belgian tax regime. The key objectives set out were to create jobs, strengthen the purchasing power and create social cohesion. The reform also needed to be budgetary neutral.

The impact of the reform will impact all taxpayers – from individual taxpayers to large multinational companies. The plan set out by the Government is indeed very broad, and below we would like to highlight a few key items that can impact companies investing in Belgium.

Note that at the time these lines are written, no (draft) law has yet been published, and our below comments are based on a preliminary understanding of the measures. Enacted measures may thus be different.

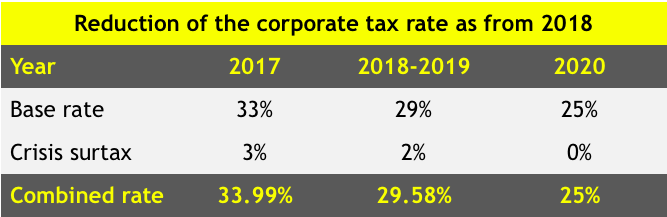

The reduction of the corporate tax rate and the limitation of the use of the tax attributes

The measures which received the most attention are the progressive reduction of the corporate income tax rate to 25% by 2020, and the limitation of the use of the tax attributes.

The gradual rate reduction – and elimination of the crisis surtax – will resolutely change the corporate tax landscape in Belgium as from 2018. The changes can be summarized as below.

Note that the SME tax rate will also be reduced as from 2018 to 20% (though the crisis surtax will be reduced at same rhythm as above) on the first EUR100,000 of taxable basis.

The Government also announced a limitation of the use of carried-forward deductions, which could lead to a minimum tax basis. Based on the Government’s plan, carried forward deductions, such as tax losses, carried-forward dividend received deduction, carried-forward innovation deduction, carried-forward notional interest deduction will be limited to EUR1m, and then to 70% of the taxable profit in excess of EUR1m. Thus even a company carrying previous years’ tax attributes could face a tax bill.

There will be however no limitation to current year’s deductions, the carry forward investment deduction and the carry forward tax credit.

Improvement of the holding regime with a 100% exemption on qualifying dividends and capital gains

The Government proposes a 100% deduction of the amount of qualifying dividends received. Currently, Belgium’s dividend received deduction regime is limited to 95% of the amount of qualifying dividends received.

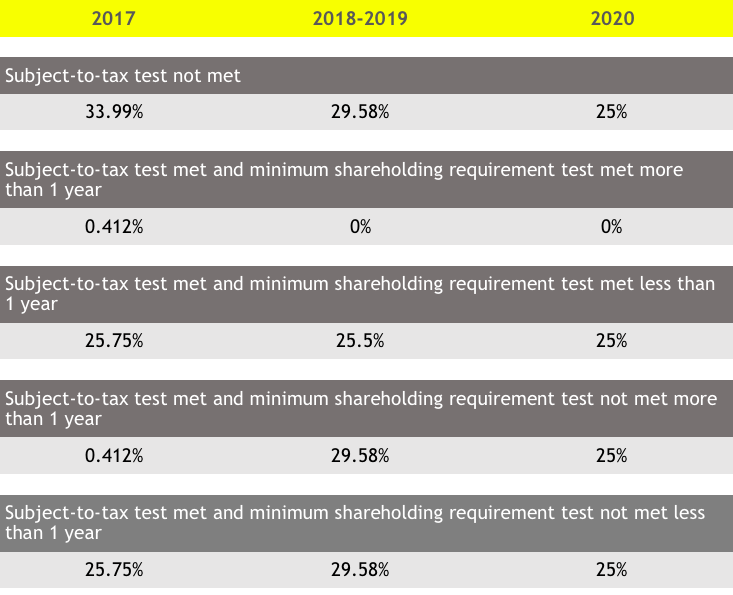

As from 2018, Belgium will (re)introduce a full exemption of capital gains on shares. Currently, realised capital gains on shares held for more than a year (where the subject-to-tax condition is met) are subject to a 0.412% taxation. This 0.412% taxation will be abolished for gains on shares held for more than one year where the subject-to-tax condition is met and the participation is of at least 10% or an investment value of EUR 2.5m – aligning the capital gain regime further on the dividend received deduction regime.

The changes to the capital gains regime can be summarized in the following table:

Reform of the notional interest deduction

The notional interest deduction regime will also be amended. The notional interest deduction regime allows for an off-balance deduction, calculated on the adjusted own equity of Belgian companies and branches, based on the average rate of the 10-year Belgian bond during the months of July, August and September of the penultimate year preceding the assessment year. For financial year 2017, this rate was of 0.237%.

As from 2018, the NID will be calculated on one fifth of the positive difference between the equity at the end of the current accounting year (“X”) and the equity at the end of accounting year five years earlier (“X-5”).It is not expected that the rest of the methodology to calculate the “NID rate” will change.

The changes to the regime reduce significantly the benefit of the regime.

Further compliance focus

In order to finance the corporate tax reform – and increase tax compliance, the Belgian Government has proposed a series of amendments which could have significant impact on taxpayers’ filing position and attitude towards the Belgian tax authorities.

- It is proposed that tax adjustments made during tax audits where a 10% penalty or more is effectively applied will constitute a minimal taxable basis for the taxpayer – no tax deduction could be offset against these (with the sole exception of current year dividend received deduction). This could potentially lead companies with losses to a cash-tax payment to be made, and will require companies with available tax attributes to consider their filing positions.

- The rate for insufficient tax prepayments will increase (in 2018 to 6.75%, from 2.25%).

- Where no corporate tax return is filed, the lump sum taxable basis will gradually increase as from 2018, leading to corporate tax due of EUR 10k.

Matching principle

As from 2018, deduction of costs in a current year whereas they belong as in reality to the following year, will be restricted – tax law will introduce the “matching principle” – and income of a following year will only be tax deductible in that year.

Provisions

As from 2018, provisions for liabilities and charges will only be tax exempt insofar they relate to contractual, legal or regulatory obligations existing at the end of the financial year.

Bearing in mind the decrease in tax rate, the Belgian Government intends to implement an anti-abuse measure – following which upon reversal, provisions will be taxed at the rate applicable at the moment they were recorded.

Tax neutral reorganizations

In line with the limitation of carried forward tax losses in the context of tax neutral reorganizations (such as mergers), any carried forward participation exemption will similarly be limited.

Anti-Tax Avoidance Directive

The EU “Anti-Tax Avoidance Directive” (so-called “ATAD”), aiming to implement across Europe the OECD and G20 recommendations on neutralizing base erosion and profit shifting (“BEPS”), will be transposed in Belgium at the occasion of the tax reform.

At this stage, little detail has been released on these very technical measures – and final legislative texts will need to be reviewed in order to be able to measure precise impact on a taxpayer’s effective tax rate.

These measures include, entering into force as from 2020:

- An interest limitation rule – limiting deduction of net interest payments above a threshold of EUR 3,000,000 to up to 30% of the EBITDA (earnings before interest, tax, depreciation and amortization). This EUR 3,000,000 is to be reviewed at a (Belgian) group level, and there will be a Public Benefit Infrastructure exemption. Disallowed interest can be carried forward;

- A “controlled foreign company” legislation will be introducing – leading to potential immediate taxation of income of subsidiaries in “low-tax” jurisdictions;

- As from 2020, the exit taxation regime will be extended in line with the Directive, and step-up will also be granted in case of transfer outside of the EU;

- The “anti-hybrid” rules as set out by the Directive are also set to be implemented in Belgium.

Tax consolidation

A tax consolidation mechanism will be introduced in Belgian tax law as from 2020. This mechanism would allow companies to make use of losses incurred by other Belgian group companies or the Belgian permanent establishment of a foreign company (under conditions), against a payment equal to the amount of tax that would have been due without this intragroup loss transfer. The regime will however not allow multiple taxpayer to be seen as one single taxpayer for tax purposes.

Historic losses incurred before 2020 will be excluded.

Disallowed expenses

The disallowed expenses regime will be further amended as from 2020, including:

- Adjustments to the company car regime, further restricting the deduction of car (and car related) expenses;

- All fines relating to direct and indirect taxes will be fully disallowed;

- The secret commissions tax will be fully disallowed and the secret commission tax rate of 50% will be abolished.

Other compensation measures as from 2020

- Limitation of losses incurred in foreign permanent establishments

Currently, losses of foreign establishments can be offset against profit of the Belgian head-office. The Government envisages to limit this – and losses of foreign PEs will only be deductible in Belgium if the losses are no longer deductible in the foreign jurisdiction. The likely outcome of this change will be that in most situations losses incurred in PEs will no longer be available in Belgium.

- Extension of the scope of the PE definition

In line with the OECD developments, the definition of PE will be broadened and aligned on the BEPS recommendations.

- Interest on “current account” positions

The reference to the market interest rate will be replaced by a reference rate based on a rate published by the Belgian national bank, increased with 2,5%, as maximum interest on debt positions without term. It is expected that an exception will be included for framework agreements for cash pooling.

Take away

The Belgian tax reform – which still needs to be translated in text of Law – will have a sweeping impact on the tax positions of multinational companies operating in Belgium.

While, the Government has presented a very significant reduction of the corporate tax rate, and further improvements to the holding companies regime, series of restrictions will also be introduced – and some of them could have a significant impact on multinational entities (CFC, interest restriction, anti-hybrids).

The reform is a step in the good direction to bring the Belgian tax rate at a more competitive level. Though a reduction to 25% still leaves Belgium in the “higher range” of European average corporate tax rates, more importance should be given to the effective tax rate. For example, this reduced rate, combined with the innovation deduction regime (which remains unchanged), will allow companies to benefit of an effective rate of 3.75% on qualifying innovative income (such as income from patents, copyrighted software, …), whereas neighbouring countries have begun increasing their tax rates on these.